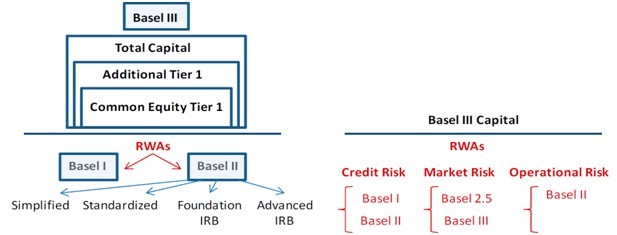

Basel III tightened the capital adequacy requirements that banks are required to observe. Common Equity Tier 1 includes instruments with discretionary dividends, such as common stocks, while additional Tier 1 includes instruments with no maturity and whose dividends can be canceled at any time. (a) The Board of Directors of each System institution shall determine the amount of regulatory capital needed to assure the System institution’s continued financial viability and to provide for growth necessary to meet the needs of its borrowers. The minimum capital standards specified in this part and part 628 of this chapter are not meant to be adopted as the optimal capital level in the System institution’s capital adequacy plan. Rather, the standards are intended to serve as minimum levels of capital that each System institution must maintain to protect against the credit and other general risks inherent in its operations. (4) A reconciliation of regulatory capital elements using month-end balances as they relate to its balance sheet in any applicable audited consolidated financial statements.

Basel II established risk and capital management requirements that ensured that banks maintained adequate capital equivalent to the risk they were exposed to through their core activities, i.e., lending, investments, and trading. (ii) The System institution has completed the applicable accounting treatment by segregating the new allocated equities from its unallocated retained earnings. The System Comment Letter questioned the value added by completing the required reconciliation on both a point-in-time and a three-month average daily balance basis.

What is Common Equity Tier 1 (CET ?

As we state above, we do not believe the proposal would increase or decrease the amount of cash patronage System institutions could pay when compared to the existing provision. The proposed changes would in no way “liberalize” the Safe Harbor or create any greater opportunity for capital distributions under the Safe Harbor. National regulators of most countries around the world have implemented these standards in local legislation. In the calculation of regulatory capital, Tier 2 is limited to 100% of Tier 1 capital. Tier 2 capital is supplementary capital, i.e., less reliable than tier 1 capital.

A bank requires tier 1 capital for general growth because the more loans they give out the the larger the amount of money they have to set aside based on the risk weighted value of the loan giving. This would have been any instrument a bank issued as a loan without requiring collateral, which was lower in priority than other debts. Basel III was designed to improve the banking sector’s ability to deal with financial stress, improve risk management, and strengthen a bank’s transparency. Basel III implementation began on Jan. 1, 2013, with a 10 percentage point reduction in Tier 3 assets every year following. Defined by the Basel II Accords, to qualify as tier 3 capital, assets must have been limited to 2.5x a bank’s tier 1 capital, have been unsecured, subordinated, and have an original maturity of no less than two years. Tier 3 capital debt used to include a greater number of subordinated issues when compared with tier 2 capital.

Tier 2 Capital

While violations of the Basel Accords bring no legal ramifications, members are responsible for implementing the accords in their home countries. Tier 3 capital is tertiary capital, which many banks hold to support their market risk, commodities risk, and foreign currency risk, derived from trading activities. Tier 3 capital includes a greater variety of debt than tier 1 and tier 2 capital but is of a much lower quality than either of the two. Under the Basel III accords, tier 3 capital is being completely abolished. (3) a minimum no-call, repurchase, redemption, or revolvement period of 5 years for tier 2 capital. Subordinated debt is debt that ranks lower than ordinary depositors of the bank.

The reserve may arise out of a formal revaluation carried through to the bank’s balance sheet, or a notional addition due to holding securities in the balance sheet valued at historic cost. Basel II also requires that the difference between the historic cost and the actual value be discounted by 55% when using these reserves to calculate Tier 2 capital. The capital that falls within the definition of Tier 2 is revaluation reserve, undisclosed reserves, hybrid security, and subordinate debt. The agreement provides limits on how much Tier 2 or Tier 3 capital can be relied upon for capital adequacy, the idea being to make sure that there is always sufficient Tier 1 capital available. Tier 3 capital consisted of subordinated debt to cover market risk from trading activities, but it is now not used in the banks of Basel Accord member countries.

One of the regulations introduced under the Basel III accord was limiting the type of capital that banks could hold in their capital structure. Banks use the different forms of capital to absorb losses that occur during the regular operations of the business. However, the financial crisis happened before Basel II could become fully effective, prompting calls for more stringent regulations to cushion against the effects of the crisis.

Upfront Financial Audit

After each successful Reg A offering, the issuer must submit for a new SEC qualification. Whereas Tier 1 Capital is commonly known as a bank’s core capital, Tier 2 Capital is known a bank’s supplementary capital. As the name insinuates, the capital that falls within this bucket is secondary to Tier 1 and is seen as being of a higher risk than its core capital partners. These are the ones that come with strings attached and no guarantee of return.

The reconciliation must include a statement that compliance with the regulatory capital requirements outlined in subpart B of this part is determined using average daily balances for the most recent 3 months. To address potential conflicts between the requirements of §§ 620.3 and 628.62(c), we proposed to revise § 620.3 to state that, unless otherwise determined by FCA, the use of the authorized limited disclosure in § 628.62(c) does not create an incomplete disclosure. We also proposed to revise § 620.3 to permit institutions to modify the required statement that the information provided is true, accurate, and complete to explain that the completeness of the disclosure was determined in consideration of § 628.62(c). In addition to minimum capital requirements, Basel II focused on regulatory supervision and market discipline. Basel II highlighted the division of eligible regulatory capital of a bank into three tiers. It includes assets such as revaluation reserves, hybrid capital instruments, and undisclosed reserves.

F. Qualified Financial Contract (QFC) Related Definitions

The overall minimum regulatory capital ratio was left unchanged at 8%, out of which 6% is Tier 1 capital. By the end of 2019, banks were required to hold a conservation buffer of 2.5% of the risk-weighted assets, which brings the total Common Equity Tier 1 capital to 7%, i.e., 4.5% + 2.5%. We are persuaded that completing the reconciliation on a point-in-time basis satisfies the Basel III Pillar 3 disclosure requirement for a reconciliation of regulatory capital to GAAP capital. We acknowledge that requiring a reconciliation on two separate bases would have added another administrative requirement.

This can vary significantly for both Tiers of offerings, but I will say that Tier 2 offerings can typically qualify faster than Tier 1 offerings. The primary distinction here is that Tier 2 offerings have a single point of qualification (which is the SEC), whereas Tier 1 offerings must meet state-level requirements which often have a higher degree of unpredictability. Under the Basel III Accords, tier 3 capital was required to be phased out starting Jan. 1, 2013, and removed from accounts by Jan. 1, 2022. Gain unlimited access to more than 250 productivity Templates, CFI’s full course catalog and accredited Certification Programs, hundreds of resources, expert reviews and support, the chance to work with real-world finance and research tools, and more. (7) Any other risk-oriented activities, such as funding and interest rate risks, potential obligations under joint and several liability, contingent and off-balance-sheet liabilities or other conditions warranting additional capital.

Consumer loan ABS fundamentals deteriorate as spreads get tighter – GlobalCapital

Consumer loan ABS fundamentals deteriorate as spreads get tighter.

Posted: Mon, 07 Aug 2023 22:09:47 GMT [source]

Subordinate debt is any type of security interest (such as bonds or stock) that hold a lower priority interest than another security. Lastly, we proposed to remove and reserve § 628.63(b)(3), which required disclosure of the computation of regulatory capital ratios during the transition period, because the provision is no longer applicable. We received no comments on this amendment and are adopting it as proposed. The System Comment Letter requested that we reconsider our position on service corporation investments. The System further noted that all service corporations are subject to chartering requirements and that FCA can establish the individual capital requirements of a service corporation on a case-by-case basis.

Understanding Tier 3 Capital

The ABA also requested that we clarify certain matters we did not expressly address in the proposal. In some cases, the ABA’s comments did not directly difference between tier 1 and tier 2 capital relate to the amendments we proposed. Tier 3 capital consisted of low-quality, unsecured debt issued by banks before the Great Financial Crisis.

- Basel II highlighted the division of eligible regulatory capital of a bank into three tiers.

- A common misconception we see is that tier I is more flexible than tier II.

- Tier 3 capital is tertiary capital, which many banks hold to support their market risk, commodities risk, and foreign currency risk, derived from trading activities.

- (2) Other than to the extent necessary for the counterparty to comply with the requirements of part 47, subpart I of part 252, or part 382 of this title, as applicable.

It is more difficult to accurately measure due because it is composed of assets that are difficult to liquidate. Often banks will split these funds into upper- and lower-level pools depending on the characteristics of the individual asset. Common Equity Tier 1 (CET1) is a component of Tier 1 Capital, and it encompasses ordinary shares and retained earnings. The implementation of CET1 started in 2014 as part of Basel III regulations relating to cushioning a local economy from a financial crisis. As discussed in Section 2—Substantive Revisions to the Capital Rule and Section 3—Clarifying and Other Revisions to the Capital Rule, the final rule adopts the revisions we proposed with minor adjustments in response to comments received. Hybrids are instruments that have some characteristics of both debt and equity.

First, we proposed to move the requirement that System associations report their tier 1 leverage ratio in each annual report for each of the last 5 fiscal years from § 620.5(f)(4)(iv) to § 620.5(f)(3)(v), as we had originally intended. In addition, we proposed to amend the requirement in § 620.5(f)(4) that institutions report core surplus, total surplus, and the net collateral ratio (banks only) in a comparative columnar form for each fiscal year ending in 2012 through 2016. This requirement resulted in System institutions reporting capital ratios beyond the 5-year requirement established in § 620.5(f), which was not our intention. Accordingly, we proposed to require these disclosures in each annual report through 2021, but only as long as these ratios are part of the previous 5 fiscal years for which disclosures are required. We received no comments on these revisions and are adopting them as proposed.

Post Offering Reporting Requirements

A bank’s total capital is calculated as a sum of its tier 1 and tier 2 capital. Regulators use the capital ratio to determine and rank a bank’s capital adequacy. Tier 1 capital is a bank’s core capital, which it uses to function on a daily basis. Tier 2 capital is a bank’s supplementary capital, which is held in reserve. The 2008 Global Financial Crisis occurred during the period when the Basel II accord was being implemented.

AngloGold’s top-tier Africa assets brought to fore, emissions cut … – Creamer Media’s Mining Weekly

AngloGold’s top-tier Africa assets brought to fore, emissions cut ….

Posted: Mon, 07 Aug 2023 09:22:00 GMT [source]

These are three (Basel I, Basel II, and Basel III) agreements, which the Basel Committee on Banking Supervision (BCBS) began to roll out in 1988. In general, all of the Basel Accords provide recommendations on banking regulations concerning capital, market, and operational risks. A bank’s tier 1 capital ratio compares its core equity assets to its risk-weighted assets. A high ratio means that the bank has enough liquid assets on hand and is more likely to absorb losses without the risk of a bank failure. We disagree with the assertion that the proposal would “liberalize” the Safe Harbor. The proposed rule would change the date for determining compliance with the Safe Harbor provision in order to simplify the administration, enforcement, and monitoring of compliance with the Safe Harbor requirements.

Financial contagion in this context would include impacts to earnings measures that are relevant to System investors and FCA’s evaluations of the safety and soundness of System institutions. We additionally proposed to revise § 628.32(l)(1) to add a provision assigning a 0-percent risk weight to gold bullion held in a System institution’s own vaults, consistent with the risk weight assigned to gold bullion held in the vaults of a depository institution. We received no comments on this revision and are adopting it as proposed. We also proposed a conforming change in § 628.20(d)(1)(i) to clarify that all instruments included in tier 2 capital must be issued and paid-in. We received no comments on this proposed change and are adopting it as proposed. The ABA asserted that the proposed rule would increase risks to the safety and soundness of the System and increase competitive inequities between the System and commercial banks.